Agricultural Finance in India: Sustainable Growth 2025

Summary: Agricultural Finance in 2025 – Empowering India’s Farming Sector for Sustainable Growth

Agricultural finance stands as the cornerstone of India’s thriving agriculture sector, especially as we approach 2025. In a nation where nearly 58% of the population relies on agriculture for livelihood, robust and sustainable financial systems are not just beneficial—they are essential. The journey toward 2025 in agricultural finance is defined by a dynamic mix of government schemes, technological innovation, and a persistent focus on sustainability. This guide delves deep into the evolving landscape of agricultural finance in India, covering everything from agricultural land finance to innovative credit products, risk management practices, and policy interventions that promote sustainable farming and empower farmers.

What is Agricultural Finance?

Agricultural finance refers to the provision of credit, loans, and financial services specially tailored to meet the unique needs of the agriculture sector. It includes funding for a broad spectrum of activities:

- Land acquisition and agricultural land finance

- Purchase of seeds, fertilizers, & modern irrigation solutions

- Investment in farm machinery and equipment

- Livestock management and expansion

- Post-harvest processing and storage

Unlike general financing, agricultural finance requires practices that directly address the cyclic, weather-dependent, and unpredictable nature of farming. Development and sustainability in Indian agriculture depend on specialized financial institutions, modern tools, and targeted government schemes to ensure access to timely and affordable finance.

Agricultural Finance in India: Current Scenario 2025

The current scenario of agricultural finance in India is shaped by a combination of institutional reforms, digital transformation, and an unwavering policy focus on sustainability. With the majority of the farming community in India consisting of small and marginal farmers, inclusive access to financial resources is more essential than ever.

- 58% of the population is engaged in the agriculture sector, making it the backbone of the economy.

- Farmers have traditionally relied on informal sources of finance—moneylenders and traders—which often led to cycles of debt and exploitation.

- Now, a robust network of banks, cooperative societies, microfinance institutions and government initiatives collectively contribute to making loans broadly accessible to the rural farming community.

In 2025, landmark schemes like the Pradhan Mantri Kisan Credit Card (PM-KCC) have been upgraded, offering lower interest rates, user-friendly application processes, and flexible repayment options. Also, major institutions such as NABARD (National Bank for Agriculture and Rural Development) play a vital role by channeling funds to grassroots rural banks and supporting sustainable farming.

Types of Agricultural Finance in India

Short-Term Funding

- Targets seasonal input needs (seeds, fertilizers, pesticides, irrigation, fuel).

- Accessible through crop loans, improving farm productivity and supporting farmers in the cyclical nature of Indian agriculture.

Medium and Long-Term Loans

- Support purchase of agricultural machinery, land development, construction of storage and irrigation infrastructure.

- Critical for boosting farm incomes and encouraging consolidation for efficiency and scale.

Agricultural Land Finance

- Focused on land acquisition, leasing and development.

- Includes specialized products encouraging sustainable land use, land improvement, and even market-driven land leasing models (a key government priority for 2025).

Microfinance and Cooperative Credit

- Empower small and marginal farmers with easier access to formal finance at grassroots level.

- Microfinance institutions and cooperative societies often design tailored products to address the unique needs of local farming communities.

Green Finance & Carbon Credit

- Promotes environmentally sustainable practices by incentivizing carbon farming, soil health, climate-smart agriculture and resource-efficient irrigation.

- Multiple public & private agricultural finance products now include carbon footprinting tools—enabling farmers and financial institutions to track sustainability KPIs and unlock green incentives.

The landscape of farming and agricultural finance in India is evolving—serving as the backbone of food security, sustainable rural development and economic resilience for the years to come.

Agricultural Land Finance: Significance and Trends

Agricultural land finance refers to credit or loan products designed specifically for purchase, leasing, development, and consolidation of agricultural land. In India, where landholdings are often highly fragmented and land use is inefficient, land finance addresses several critical challenges:

-

Facilitates consolidation:

Increases the size of operational holdings, encourages large-scale sustainable farming, and enables the adoption of advanced technology. -

Promotes sustainable land use:

Targeted financing supports land improvement, adoption of climate-smart practices, and resource-efficient cropping patterns. -

Unlocks land leasing markets:

By providing finance for leasing, both landowners and tenants can benefit from structured agreements and incentives to follow best practices. -

Integrates technology:

Agricultural land finance products now use satellite-driven valuation, AI risk assessment and blockchain-based traceability, ensuring fair disbursal and transparent processing.

With digital transformation in 2025, schemes in India are moving toward the model seen in UK agricultural finance—emphasizing sustainability, environmental stewardship, and robust monitoring of land use.

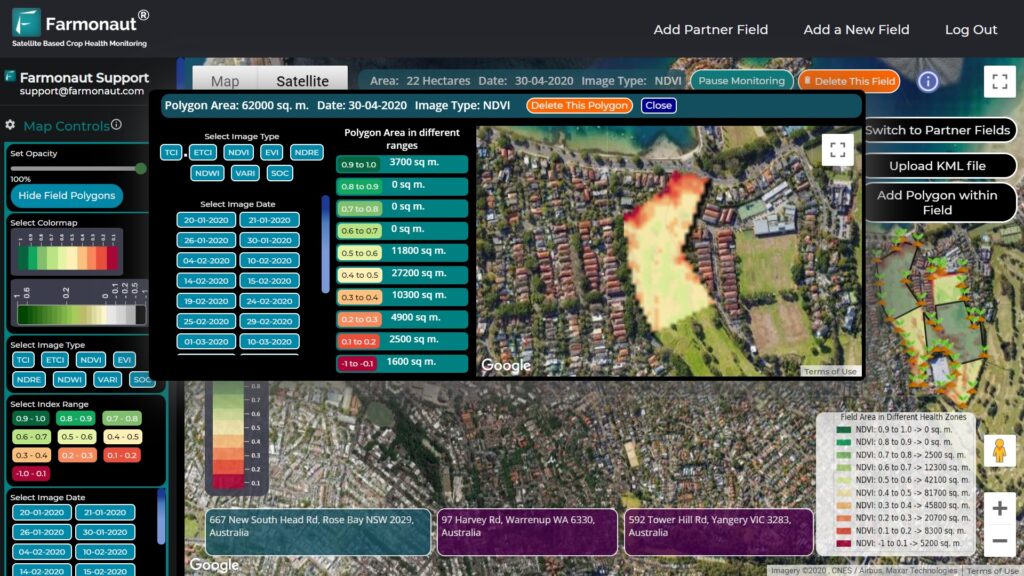

Discover more about satellite-powered land use analytics and monitoring in agriculture with the video below, relevant to emerging traceability platforms and transparent supply chains:

The Role of Technology in Agricultural Finance: Farmonaut’s Satellite-Driven Future

As we journey towards sustainable growth in Indian farming and agricultural finance, technology-led transformation is at the core of every major policy and business strategy. Farmonaut, as a leader in satellite-based solutions, is powering this revolution by providing affordable, scalable, and cutting-edge data-driven tools to banks, financial institutions, businesses, farmers, and government agencies.

-

Satellite Monitoring: Our platform leverages multi-spectral satellite imagery to monitor

- Land conditions and crop health (NDVI)

- Soil quality and moisture for risk assessment

- Farm boundaries, lease areas, and improvements

These tools guide both lenders and borrowers in rural India for more accurate and dynamic credit appraisal.

- AI-Based Advisory: The Jeevn AI System delivers real-time, location-specific insights, weather forecasts, and risk warnings. It empowers farmers with science-backed strategies for productivity, while helping institutions manage agricultural loan portfolios efficiently.

- Blockchain Traceability: Our blockchain traceability solutions secure every step of the agricultural supply chain—making transaction histories tamper-proof, boosting transparency, and reducing loan fraud.

- Environmental Impact & Carbon Tracking: Farmonaut supports carbon footprinting and resource use analytics, a key component for green lending products and compliant sustainable agriculture.

- Loan & Insurance Verification: Financial institutions utilize our satellite-based crop loan & insurance verification services to minimize default risk, validate land use, and facilitate timely disbursal of farm credit.

Our Solutions for Every Stakeholder:

- Farmers: Gain actionable insights to optimize productivity, meet sustainability benchmarks, and access tailored advisory for better practices and improved credit profiles.

- Financial Institutions: Use satellite data for accurate borrower verification and risk monitoring, thus expanding the agricultural loan portfolio securely and sustainably.

- Government Agencies: Plan, monitor, and evaluate agricultural development programs on a macro scale using real-time, region-wise satellite insights.

- Businesses & Corporate Enterprises: Track supply chain sustainability with blockchain-based traceability, ensuring environmental compliance and consumer trust.

With a powerful blend of AI, machine learning, and user-friendly interfaces across web, Android, and iOS, Farmonaut democratizes satellite technology for everyone. Explore fleet management and large-scale farm management for streamlined logistics and enterprise-scale monitoring in agriculture.

Key Government Institutions and Schemes (2024–2025)

The government of India, recognizing the critical role of agricultural and land finance, has introduced significant schemes to promote a sustainable financial ecosystem and support the farming sector in 2025 and beyond:

- Pradhan Mantri Kisan Samman Nidhi (PM-KISAN):

Direct income support to eligible farmers, coupled with credit linkages. - Pradhan Mantri Kisan Credit Card (PM-KCC):

Upgraded for 2025—offers flexible, low-interest crop loans with streamlined digital applications. - NABARD Refinance Schemes:

The National Bank for Agriculture and Rural Development plays a pivotal role in channeling funds to rural banks, cooperatives, and microfinance institutions for sustainable agriculture. - Interest Subvention Schemes:

Reduce effective loan rates helping farmers access cheaper credit for vital activities. - Green Financing Initiatives:

Include carbon credit incentives, resource conservation financing, and environmental stewardship compliance as a requirement for funding in 2025. - PMFBY (Pradhan Mantri Fasal Bima Yojana):

Bundled crop insurance schemes linked with credit products, protecting farmers against climatic and price risks. - Private Sector & NBFC Agri-Loans:

Offer bespoke financial products focusing on land consolidation, precision irrigation, and digital monitoring.

The collective impact of these schemes is a rural landscape where farmers have easier access to credit; banks are empowered to take smarter risks, and sustainable agricultural practices are incentivized at scale.

Comparison Table of Key Agricultural Finance Schemes (2024–2025) and Their Impact on Sustainability

| Scheme Name | Type of Finance | Estimated Funding Amount (₹ crore) | Year of Launch/ Implementation | Key Eligibility Criteria | Focus Area | Estimated Beneficiaries (2025 projection) |

|---|---|---|---|---|---|---|

| PM-KISAN | Income Support, Credit Linkage | ₹70,000+ | 2019 (Upgraded 2024) | All small & marginal farmers | Sustainability, Inclusion | ~10 crore |

| PM-Kisan Credit Card (PM-KCC) | Crop Loans, Working Capital | ₹8,00,000+ | 1998 (Upgraded 2025) | Registered cultivators | Inclusive Credit, Tech Use | ~6 crore |

| NABARD Refinance Schemes | Land, Equipment, Crop, Infra | ₹4,50,000+ | 1982 (Annual/ Ongoing) | Rural banks, MFIs, Co-ops | Rural Dev, Tech, Sustainability | ~12 crore |

| PM Fasal Bima Yojana (PMFBY) | Crop Insurance | ₹50,000+ | 2016 (Revised 2024) | Insured & KCC-linked farmers | Risk, Sustainability | ~5 crore |

| Green Finance Initiatives | Carbon, Resource Use | ₹8,000+ | 2023–2025 | Green compliance, agri tech use | Environment, Tech, Carbon | 1+ crore |

| Private/NBFC Land Finance | Land Purchase, Leasing, Mechanization | ₹12,500+ | 2018+ (Expanding 2024+) | Land-eligible, creditworthy | Tech, Consolidation | 80 lakh |

Innovations in Agriculture Financing 2025 and Beyond

With rapid digitalization, agricultural finance in India is transforming like never before—moving beyond traditional lending to create a resilient and future-proof rural economy. Key breakthrough innovations in 2025 include:

-

Agri-Fintech Platforms:

Mobile apps and online portals simplify access to loans, insurance, subsidies, and market linkages. Farmers receive real-time approvals, transparent tracking, and instant advisory. -

Data-Driven Credit Assessment:

Use of satellite imagery, machine learning, and weather analytics for precision farm profiling, yield prediction, and tailored finance products. -

Integrated Insurance and Credit:

Bundled loan-insurance products safeguard farmers from climate vagaries, reducing repayment risk and NPAs for banks.

Explore satellite crop loan & insurance verification >> -

Blockchain in Agri-Finance:

Enables tamper-proof identity, record-keeping, and traceability, essential for large farm holdings and premium/organic markets. -

Climate & Carbon Financing:

Access to international carbon credits, incentivizing conservation farming and resource-efficient practices with measurable environmental outcomes.

Get started with carbon footprinting >>

Challenges and Future Outlook

Despite immense progress, certain challenges in agricultural finance in India remain:

- Low credit penetration in remote and marginalized regions persists despite widespread institutional reforms and fintech innovation.

- Climatic risk, environmental shocks, and unpredictable rainfall continue to impact crop production and farmers’ ability to repay loans.

- Financial literacy gaps limit understanding and uptake of advanced products, especially insurance and digital lending.

- Risk of non-performing assets (NPAs) in agri-lending continues as a deterrent for banks and private sector lenders.

- Fragmented landholdings and rigid tenancy laws hinder the scaling up of sustainable agricultural practices in many states.

- Environmental sustainability mandates, while beneficial, require rigorous assessment and reporting tools—made possible through satellite monitoring, AI, and blockchain.

Overcoming these challenges calls for deeper integration of satellite technology, AI-powered advisory, and collaborative public-private efforts that focus on sustainable, inclusive growth.

The Future: Resilient & Sustainable Agri-Finance Systems

- Widespread digitization—businesses, banks, and farmers will transact, monitor, and manage loans end-to-end digitally.

- Data-driven risk management—with high-resolution, real-time satellite and weather data, lending in rural India is becoming hyper-local and responsive to on-ground changes.

- Financial inclusion—new product designs, micro-loans, and green finance ensure coverage for the smallest stakeholders.

- Climate-smart financing—banks, NBFCs, and government schemes will increasingly link disbursal to sustainability criteria.

- Scalable satellite solutions—tools like ours (Farmonaut) are scalable from individual farmers to large agri-corporates, ensuring everyone benefits from digital transformation.

Farmonaut Subscription Packages

To make satellite-powered agriculture accessible for everyone—individual farmers, businesses, government agencies, and financial institutions—our Farmonaut subscription packages provide a cost-effective, scalable way to integrate precision monitoring, advisory systems, fleet management, and large-scale farm management—directly into your agricultural and financial operations.

FAQ: Agricultural Finance in India 2025

What is agricultural finance?

Agricultural finance refers to specialized credit, loans, and financial services tailored to meet the diverse needs of farmers and the agricultural sector. It supports activities like land acquisition, input purchase (seeds, fertilizers, etc.), machinery buying, livestock management, and post-harvest processing—addressing the unique, cyclic, and weather-dependent nature of farming.

How is agricultural land finance different from other types of farm finance?

Agricultural land finance focuses on loans and credit products specifically for the purchase, leasing, or development of farmland, encouraging consolidation and sustainable land use. It differs from general crop loans or seasonal funding by being tailored for property acquisition and long-term improvements, often integrated with satellite-driven valuation tools in India by 2025.

Which are the key institutions and government schemes for farm finance in India?

Top institutions and schemes include NABARD (National Bank for Agriculture and Rural Development), Pradhan Mantri Kisan Credit Card (PM-KCC), PM-KISAN direct benefit scheme, PMFBY (crop insurance), and various state and private sector financing initiatives—all focused on boosting access and promoting sustainable, technology-driven farming practices.

How does technology benefit agricultural finance in India?

In 2025, innovative platforms such as Farmonaut use satellite imagery, AI, machine learning, and blockchain to:

- Enable accurate land and crop monitoring for loan assessment

- Provide real-time credit, insurance, and risk management insights

- Facilitate transparency and traceability in supply chains

- Encourage sustainable land use by tracking environmental impact/carbon footprint

These advances benefit farmers, banks, lenders, and government agencies alike.

How can Indian farmers access affordable credit for sustainable agricultural growth?

Farmers should explore government schemes like PM-KCC, approach cooperative societies and regional rural banks, and utilize digital agri-fintech platforms offering tailored loan and insurance products. Integrating carbon tracking and traceability can unlock additional green incentives and lower rates for sustainable practices in 2025.

What role does sustainable finance play in the future of agriculture?

Sustainable finance incentivizes the adoption of environmentally responsible, climate-smart agricultural practices by linking credit with measurable sustainability outcomes—such as soil health, water management, resource optimization, and carbon sequestration. This is essential for long-term food security, rural development, and global environmental goals.

Are advancements in agricultural finance in India comparable to trends in UK agricultural finance?

The Indian agricultural finance landscape is converging with global trends, including UK agricultural finance, emphasizing sustainability, digital integration, and robust risk management. However, India’s scale, diversity, and smallholder focus require localized product innovation, broader financial inclusion, and technology-driven solutions.

Conclusion: Pathway to Sustainable Growth in Indian Agriculture

Agricultural finance in India will continue to empower farmers, foster sustainable growth, and transform the country’s agricultural and rural landscape through 2025 and beyond. Innovative use of credit, land finance, and technology ensures risk mitigation, higher productivity, and environmental stewardship.

The future holds tremendous promise, with government and private sector investments converging on sustainable, inclusive, and technology-driven solutions. By embracing modern agri-fintech platforms, investing in green lending, and leveraging satellite-data-driven services (like those provided by Farmonaut), the Indian farming sector is well positioned for resilience, prosperity, and global leadership in sustainable agriculture.

Let’s continue to champion a future where every farmer in India has the means, knowledge, and tools to thrive sustainably, securing the nation’s food security, economic vitality, and environmental health for generations to come.

For more information and to get started with affordable, satellite-driven insights for your land, farm, or organization, download the Farmonaut App today.