Farm Loans & Ag Loans: 7 Powerful Funding Options for 2026

- Introduction: Farm Loans & Ag Loans in 2026

- The 2026 Landscape: Agricultural Financing Overview

- 7 Powerful Farm Loan & Ag Loan Options for 2026

- Farm Loans Comparative Table: Features & Rates for 2025–2026

- Harnessing Technology for Better Farm Financing: Farmonaut’s Role

- Farm Loan Application Process & Best Practices

- Frequently Asked Questions (FAQs) on Farm & Ag Loans

- Conclusion: Navigating the Future of Agricultural Finance

“Over 60% of new farm loans in 2025 are projected to be USDA-backed, supporting sustainable agricultural practices.”

“Farm land loans in 2025 are expected to fund more than 200,000 acres of agricultural expansion across the U.S.”

Introduction: Farm Loans & Ag Loans in 2026

As we approach 2026, the agricultural financing sector continues to evolve, offering a variety of farm loans, ag loans, farm land loans, and USDA farm loans tailored to meet the needs of farmers, ranchers, and agricultural entrepreneurs. The rising complexities of farming—from climate change, supply chain disruptions, to fluctuating commodity prices—make financial support and flexible loan options more crucial than ever for maintaining productivity, sustainability, and profitability.

Understanding the distinctive options and eligibility criteria for 2026’s agricultural loan products is essential for anyone involved in agriculture seeking to expand, modernize, or sustain operations. Whether your farm requires funding for arable land, livestock, equipment, or sustainable technology, the loan landscape is ripe with solutions for every type of operation.

The 2026 Landscape: Agricultural Financing Overview

The farm loans sector is a rapidly shifting landscape, influenced by environmental concerns, technological advances, market volatility, and evolving government policy. Both public and private lenders are recognizing the need for flexible financial support that aligns with modern agricultural realities—primarily focusing on sustainability, innovation, and resilience.

Why Are Farm Loans in 2026 More Important Than Ever?

- Climate Adaptation: Extreme weather, droughts, and shifting precipitation patterns demand capital for climate-smart investments.

- Supply Chain Fluctuations: Recent disruptions in global supply chains make access to seasonal operational funds critical for continuity in farming and ranching operations.

- Technology & Modernization: Innovations such as AI, remote sensing, and automation require continuous investment in equipment and infrastructure.

- Environmental Stewardship: Lenders are increasingly offering better terms and incentives for adoption of sustainable practices and conservation projects.

- Sustainable Growth: Agricultural growth must address rising land prices and competition, especially for new and beginning farmers.

7 Powerful Farm Loan & Ag Loan Options for 2026

Let’s break down the broad category of farm and ag loans available for 2026. This comparative guide helps farmers, producers, ranchers, and agricultural entrepreneurs determine which funding options best match specific operational and growth needs.

1. USDA Farm Loans

The USDA (United States Department of Agriculture) is expected to remain a cornerstone in agricultural financing through 2026, especially for family farms, beginning farmers, and underserved rural groups. USDA farm loans come as both direct and guaranteed loans, offering some of the lowest interest rates and longest repayment terms in the sector.

- Loan Programs Include:

- Farm Ownership Loans (purchase, expand, refine, or improve farmland)

- Operating Loans (seeds, fertilizer, equipment, livestock, and working capital)

- Microloans (small farm and niche operations support)

- Farm Storage and Facility Loans

- Conservation Loans

- Eligibility: U.S. citizenship or legal residency, farming experience, fair credit history, and viable repayment plan.

- Special Features: Programs for beginning farmers, veterans, and socially disadvantaged applicants. Increasing integration of climate-smart agriculture incentives for environmental resilience.

For those seeking streamlined processes for crop loans and insurance using satellite-based verification, explore our Crop Loan & Insurance Solutions. These tools are designed to support both financial institutions and farmers with accurate, real-time data for faster approvals and reduced risk.

2. Farm Land Loans

Farm land loans are designed specifically for those needing finance for the purchase, refinance, or expansion of farmland. With agribusinesses and independent farmers competing for prime arable land, these loans remain a cornerstone for operational expansion.

- Loan Uses: Buying new farmland, refinancing existing agricultural properties, developing renewable energy installations, or investing in conservation projects.

- Loan Structure: Long-term (often up to 30 years), fixed or variable interest rates, frequent down payment requirements, collateral (typically the land itself).

- Eligibility Emphasis: Proven production history, sound business plan, environmental stewardship (offering better terms for sustainable farming or solar installations).

Learn how our Carbon Footprinting Tools and Traceability Solutions can enhance your eligibility by demonstrating environmental sustainability and compliance to lenders.

3. Small Farm Loans

Small farm loans provide crucial opportunities for beginning, niche, and specialty crop farmers. With lower loan thresholds and tailored technical assistance, these products empower newcomers and local, rural entrepreneurs to establish viable agricultural businesses.

- Typical Borrowers: Operations under 100 acres in size, specialty or value-added producers, urban agriculture projects, and underserved communities.

- Support Services: Financial education, farm management advisory, and business coaching. In 2026, lenders are enhancing technical resources to help maximize the impact of borrowed funds.

- Popular Providers: USDA Microloans, Farm Service Agency programs, agricultural credit unions, and local community development financial institutions (especially when searching for “farm loans near me”).

4. Sustainable Agriculture Loan Programs

With environmental stewardship growing ever-more central to agriculture, an increasing number of farm loans and ag loans are dedicated to projects promoting soil health, water management, biodiversity, and climate resilience.

- Loan Uses: Funding for carbon reduction practices, regenerative farming techniques, solar and wind energy installations, and ecological restoration of arable or pasture lands.

- Special Features: Lower interest rates, loan forgiveness for measurable environmental outcomes, and government or NGO-backed incentives.

- Typical Providers: Major banks with ag lending arms, USDA Conservation Loan Program, State-level green loan initiatives.

Learn more about our Carbon Footprinting and Product Traceability services for tracking sustainable farming and gaining incentives from environmentally oriented lenders.

5. Local and Regional Bank Ag Loans

When searching for farm loans near me, local and regional banks or credit unions remain among the most accessible lenders for customized farm loans and ag loans. Their familiarity with local crop patterns, soil types, seasonal weather, and commodity markets allows for more tailored credit solutions.

- Key Benefits: Personalized service, quicker loan decisions, and flexible repayment schedules aligned with the harvest cycle.

- Loan Types: Seasonal operating lines of credit, farm land loans, small farm loans, and equipment financing.

- Eligibility: Demonstrated agricultural experience, strong local references, sound business plan, and sometimes community involvement.

6. Farm Equipment Loans

Modern farms and ranches require advanced equipment to maintain competitiveness and increase resilience. Farm equipment loans are flexible loans used to buy new or upgrade tractors, implements, irrigation systems, and precision agriculture technology.

- Loan Coverage: Purchases, leases, or even retrofits on existing machinery.

- Repayment Structure: Typically mirrors machine depreciation periods, often with flexible payment schedules to help offset seasonal income patterns.

- Providers: Regional ag banks, equipment manufacturers’ finance arms, and credit unions.

-

Optimize with Fleet Management:

Discover Fleet Management Solutions to track, manage, and optimize your equipment investments efficiently through AI and satellite-driven insights.

7. State/Federal-Backed and Alternative Lending Programs

Beyond core programs, a range of state, federal, and private sector-backed agricultural loans are available to fill specific financing gaps or address unique needs, such as:

- Young and beginning farmer grants and loans

- Disaster relief and emergency operating loans

- Loans for specialty crop innovation and urban farming

- Agricultural technology and modernization loan funds

For large-scale farm management and digital transformation, explore our Large-Scale Farm Management Platform, designed to support efficiency and compliance for expanding operations.

“Over 60% of new farm loans in 2025 are projected to be USDA-backed, supporting sustainable agricultural practices.”

“Farm land loans in 2025 are expected to fund more than 200,000 acres of agricultural expansion across the U.S.”

Farm Loans Comparative Table: Features & Rates for 2025–2026

| Loan Type | Interest Rate Range (%) | Maximum Loan Amount | Eligibility Requirements | Repayment Term (Years) | Special Features |

|---|---|---|---|---|---|

| USDA Direct Farm Loan | 2.5% – 4.0% | $600,000 (ownership); $400,000 (operating) | U.S. citizen/resident, meet ag experience, credit, and income criteria | 10–40 | Climate-smart initiatives, support for underserved/beginning farmers |

| USDA Guaranteed Farm Loan | 4.5% – 6.8% | $2,037,000 | Meet USDA and commercial lender standards | 7–30 | 80%-90% loan guarantee; lower down payments |

| Farm Land Loan (Conventional Bank) | 5.0% – 7.5% | $5,000,000+ | Land as collateral, business plan, credit check, down payment | 10–30 | Better rates for conservation/renewable energy projects |

| Small Farm/Microloan | 3.0% – 4.5% | $50,000 | Beginning/small farm, business plan, basic farming experience | 1–7 | Technical assistance, streamlined process |

| Sustainable Agriculture Loan | 2.8% – 5.2% | $250,000–$3,000,000 | Environmental plan, sustainability practices | 5–20 | Incentives for carbon reduction, lower rates for green projects |

| Local Bank/Regional Credit Union Ag Loan | 4.5% – 8.5% | $500,000–$10,000,000 | Local residency, community ties, crop/livestock plan | 3–25 | Flexible repayment, seasonal scheduling |

| Farm Equipment Loan | 5.0% – 9.0% | Up to 100% equipment value | Pro-forma financials, equipment quote | 2–7 | Fast approval, tied to equipment lifespan |

| State/Federal Ag Grants & Alternative Loans | Varies, often subsidized | $20,000–$1,000,000+ | Targeted to project type (e.g., disaster, beginning, innovation) | 1–15 | Partial forgiveness, innovation bonuses |

Harnessing Technology for Better Farm Financing: Farmonaut’s Role

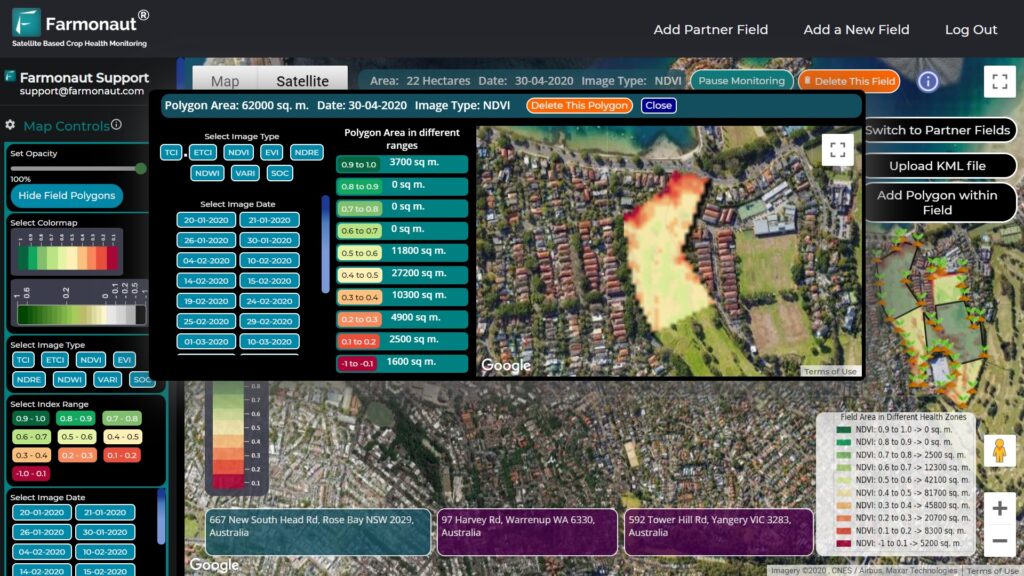

Robust, reliable data is pivotal in today’s agricultural loan processes. At Farmonaut, we empower lenders and borrowers by providing satellite-driven insights, AI-powered advisory, and blockchain traceability through our mobile, web, and API solutions.

- Satellite-Based Crop Monitoring: Real-time, multispectral imagery tracks vegetation health, soil conditions, and field productivity—vital proof for loan or insurance claims.

Learn how satellite verification streamlines crop loans & insurance. - AI Advisory and Jeevn AI: Cut through the noise with data-driven recommendations for sustainable land management, input planning, and risk reduction—enhancing loan eligibility and performance.

- Blockchain Traceability: Build supply chain transparency—a valuable asset for qualifying for some sustainable ag loans and traceability-linked financing.

Explore Farmonaut’s blockchain-based traceability solutions here. - Fleet & Resource Management: Optimize equipment investments with smart tracking, helping you justify funding requests and ensure lender transparency.

See our fleet management capabilities. - API & Developer Tools: For agribusinesses and banks needing integration, our API delivers crop data directly to your platform.

Consult our API Developer Docs for fast onboarding.

Our modular subscription-based offering (see options below) ensures scalable solutions for individual farmers, large agribusinesses, and government institutions, regardless of operational size or location.

Farm Loan Application Process & Best Practices (2026 Edition)

The path to securing farm loans, farm land loans, ag loans, and USDA farm loans in 2026 involves both preparation and strategic decision-making. Below is a stepwise summary to streamline your loan journey:

- Identify the Loan Purpose: Land purchase, operational costs, equipment, sustainable investment, expansion, or refinancing?

- Assess Eligibility: Check your experience, credit rating, farm size, business plan, and—where relevant—alignment with environmental or new farmer incentives.

- Gather Documentation:

- Tax returns (3+ years recommended)

- Farm production and income records

- Business plan with projections

- Collateral appraisals (for land, equipment, or livestock loans)

- Environmental, sustainability, or conservation plans (for green loans)

- Shop Loan Options: Explore USDA, banks, credit unions, and state agencies. If possible, compare rates using tables like the one above.

- Consider Technology Integration: Use Farmonaut’s monitoring and reporting tools to generate field data that may streamline approval or secure sustainability incentives.

- Submit Application: Follow lender’s checklist, complete financial statements, and explain unique farming risks or strategies.

- Prepare for Review and Approval: Respond quickly to lender queries—especially those about environmental impacts, repayment sources (e.g., crop income), and technology adoption.

- Close and Manage the Loan: Use digital dashboards (including Farmonaut’s offerings) to track progress, meet milestones, and simplify reporting for subsequent years or renewals.

For those investing in forestry, carbon farming, or adopting regenerative practices, see how the Crop, Plantation, & Forest Advisory Platform helps maximize yields while qualifying for climate-linked finance.

Frequently Asked Questions (FAQs) on Farm & Ag Loans

- What are the best farm loans for beginning farmers in 2026?

- USDA Farm Loans and Small Farm/Microloans are excellent, as they offer low interest rates and support for those with limited credit. State and nongovernmental programs also provide grants and technical assistance targeting first-time operators.

- How can sustainable practices help me secure better farm land loan terms?

- Demonstrating soil health initiatives, renewable energy use, or conservation efforts can make your application stand out—and often qualifies you for lower interest and special incentives.

- Where do I find “farm loans near me” for special crops or unique environments?

- Local and regional banks, credit unions, and USDA offices are the best first stops. Search your state’s agriculture department for niche programs, especially for specialty or organic production.

- Can I use farm loans for technology investments?

- Yes! Many ag loans and equipment loans in 2026 cover precision ag tech, remote monitoring systems, farm management software, and sustainability reporting platforms—like those from Farmonaut.

- What if my income varies seasonally—will lenders accommodate?

- Absolutely. Most agricultural loan repayment schedules are aligned with harvest seasons, and lenders can structure installments around your farm’s cash flow cycles.

- Are there loans specifically for organic, regenerative, or carbon farming?

- Yes. USDA’s Conservation Loans, various sustainable ag loans, and some credit unions now offer products specifically for environmentally conscious operations, with incentives for measurable ecological benefits.

- How does technology help with getting approved?

- Integrating proof from satellite-based crop monitoring or resource management systems (like those from Farmonaut) offers lenders transparent data, reducing approval times and increasing confidence in your project’s likely success.

Conclusion: Navigating the Future of Agricultural Finance

In an era marked by rapid change and fierce competition, the right approach to farm loans, ag loans, farm land loans, and USDA farm loans is key to building a resilient and thriving operation. We’ve seen how 2026’s agricultural lending landscape is increasingly accommodating sustainability, modernization, and inclusivity.

- Explore multiple loan products.

- Align your financing with business goals—whether expanding land, adopting new tech, or going green.

- Rely on digital tools (like Farmonaut) to manage applications and strengthen lender confidence.

- Continue developing resilient, future-focused farms—using smart, tailored funding options for every challenge.

To maximize the benefits of the most powerful farm loans and ag loans for 2026, stay informed, leverage new technology, and be proactive in seeking the programs that align best with your mission. The future of American agriculture depends on both innovation and wise, accessible financing.