Farmland Loan Rates 2025 & Terms for Smart Buying

In the evolving agricultural landscape of 2025, farmland loan rates and farmland loan terms are central to the success of farmers, land investors, and agribusinesses alike. This comprehensive article explores the latest farmland loan opportunities, essential considerations for securing a loan to buy farmland, and actionable insights for thriving in today’s dynamic market. We examine rates, terms, and innovations in farming loan products—equipping you with the knowledge to make smart, sustainable land purchases and enhance your operations.

Overview: Farmland Loans’ Role in Agricultural Sector 2025

As we move into 2025, access to affordable farmland loan options continues to play a pivotal role in supporting the agricultural sector, empowering farmers and agribusinesses to expand operations, adopt innovative practices, and enhance productivity. With the demand for food ever-increasing—alongside the mounting challenges posed by climate change, evolving market dynamics, and rising input costs—the right financing can mean the difference between stagnation and growth.

This article provides an in-depth exploration of farmland loan rates, loan terms, and practical considerations for securing a loan to buy farmland in 2025, guiding entrepreneurs, farmers, and investors towards informed, resilient decisions.

“Average farmland loan rates in 2025 are projected to range between 5.2% and 6.8% across major U.S. regions.”

Understanding Farmland Loans: Essential Background

Farmland loans are a specialized type of financing designed for the purchase, improvement, or refinancing of agricultural land. Unlike traditional home loans, these offerings are built around the unique conditions and factors inherent to agriculture—including soil quality, water availability, crop yield history, and the experience of the borrower.

- Farmland loans are obtained through commercial banks, agricultural finance institutions, specialized credit unions, and government-backed programs.

- Lenders assess risk based on the specific characteristics of a farm or land parcel, often requiring more detailed management plans than residential mortgages.

- Terms are tailored to support not only productivity and growth, but also sustainability and risk mitigation in a volatile sector.

In addition to purchase loans, farming loan products may include funds for:

- Land improvement projects (drainage, fencing, conservation)

- Adoption of sustainable practices (organic certification, regenerative agriculture)

- Farm refinance (to consolidate debts or finance new ventures)

- Large-scale management (see Farmonaut Large Scale Farm Management for technology-supported farm oversight)

Farmland Loan Rates in 2025: Key Trends & Influences

Farmland loan rates in 2025 have seen moderate fluctuations in response to broader economic trends, inflation, and central bank policies. Following a period of historically low rates during earlier years, 2025 rates have stabilized, sitting on average between 5% and 7% for most U.S. agricultural loan applicants.

- This range strives to balance controlling inflation with the need to support rural growth and farm ownership.

- Lenders often offer preferential rates for projects that actively enhance environmental stewardship, such as sustainable farming or land conservation.

- Interest rates for farmland loans may vary, depending on multiple factors:

- Borrower creditworthiness (credit score, financial history)

- Size of loan request and value of collateral land

- Profitability and cash flow projections of the farm operation

- Government programs or subsidies can reduce effective rates in special cases

In some regions, government or state-backed loan programs continue to serve as important levers for accessibility. These programs may offer additional subsidies, reduced rates, or relaxed eligibility criteria—especially aimed at beginning farmers, family operations, or land improvement efforts.

Comparative Table: 2025 Farmland Loan Terms & Rates

For a quick overview, here’s a comparative reference highlighting typical interest rates, repayment terms, down payment requirements, and special notes for each major farmland loan provider category for 2025.

| Lender Type | Estimated 2025 Interest Rate (%) | Typical Loan Term (Years) | Minimum Down Payment (%) | Typical LTV Ratio (%) | Special Conditions / Notes |

|---|---|---|---|---|---|

| Agricultural Banks | 5.5 – 6.8 | 10 – 25 | 20 – 30 | 65 – 80 | Competitive rates based on farm’s cash flow; incentives for sustainability projects |

| Credit Unions | 5.2 – 6.5 | 10 – 20 | 15 – 25 | 70 – 85 | Often lower fees; localized support for regional borrowers |

| Government Programs (e.g., USDA, state ag loan programs) | 5.0 – 6.0 | 12 – 30 | 5 – 20 | 80 – 95 | Possible rate reductions, grants, or insurance for young/beginning farmers |

| Private Lenders | 6.8 – 7.5 | 5 – 15 | 25 – 35 | 60 – 75 | May offer rapid closing; often higher rates due to increased risk tolerance |

“Typical farmland loan terms in 2025 span 10 to 30 years, supporting long-term business planning for entrepreneurs.”

“Typical farmland loan terms in 2025 span 10 to 30 years, supporting long-term business planning for entrepreneurs.”

Loan to Buy Farmland: Key Considerations & Steps

Obtaining a loan to buy farmland in 2025 requires strategic preparation and careful evaluation of both financial and agricultural factors. Here are the key considerations and steps when seeking farmland financing:

1. Establish Your Financial and Operational Readiness

- Prepare a detailed business plan, outlining projected cash flow, management experience, and intended sustainable practices.

- Assess personal and farm creditworthiness. Lenders often require strong credit history, debt serviceability, and collateral assets.

- Gather all required documentation, including property records, water/land rights, environmental impact analysis, and conservation plans.

- Evaluate down payment capacity—be ready to invest 15-30% up front based on loan product.

2. Conduct Rigorous Due Diligence on Land

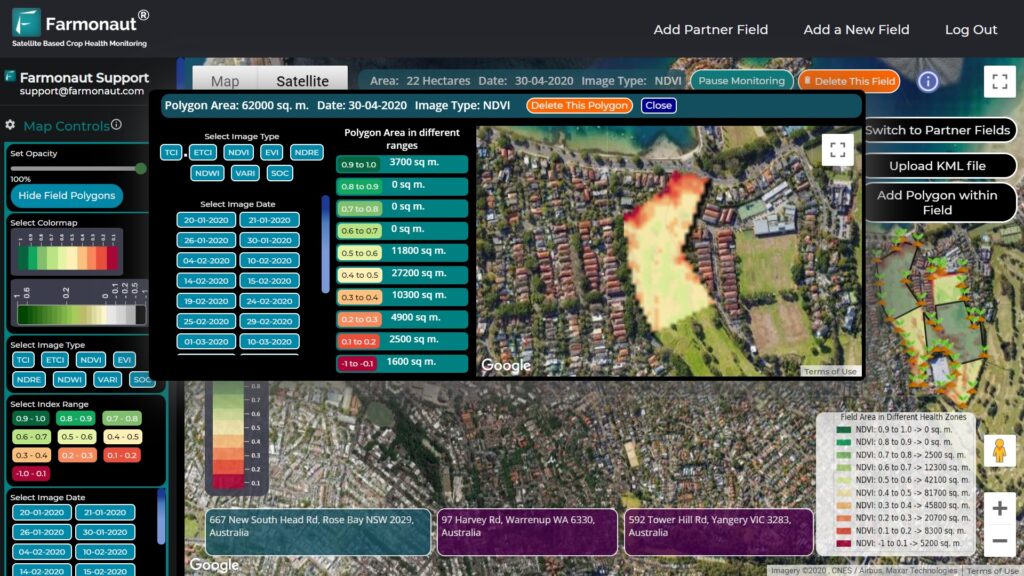

- Thoroughly assess soil quality (using soil health data and remote sensing, for example via Farmonaut’s Large Scale Farm Management App).

- Verify water availability & rights; check current irrigation systems and legal constraints.

- Inspect infrastructure: fencing, outbuildings, proximity to key markets and processing facilities.

- Document access routes, zoning issues, and neighborhood land use trends.

3. Analyze Market and Policy Climate

- Track local and global food demand, regional agricultural trends, and export/import policy risks.

- Keep abreast of climate change risks and evolving input costs—consider farms resilient to future weather events and commodity price volatility.

- Take advantage of government programs or cooperatives that may offer loan guarantees, subsidies, or special terms.

4. Secure and Negotiate the Best Loan

- Shop around—compare rates, terms, and special conditions from banks, credit unions, government-backed and private lenders.

- Negotiate for flexible terms that accommodate agricultural cash flow cycles, such as seasonal payment breaks or interest-only periods for initial years.

- Consider value-added financing, such as preferential rates for implementing carbon footprint reduction projects, or leveraging blockchain-based product traceability for premium market positioning.

Farmland Loan Terms: What to Expect in 2025

Farmland loan terms in 2025 provide flexibility and adaptability to accommodate both small-scale and large-scale agricultural operations:

Term Lengths & Structures

- Repayment periods usually range from 5 to 20+ years. Some programs stretch to 30 years, supporting generational family farming.

- Amortization: Most farmland loans are amortized with equal monthly payments, but interest-only periods (especially first 3-5 years) are available to support initial operational needs.

- Renewal & Extension: Many lenders allow for term renewal or refinancing, letting borrowers adjust when economic or operational circumstances shift.

- Prepayment Penalties: Review whether your loan incorporates penalties/fees for early payoff. Negotiate where possible for flexible prepayment.

Collateral & Loan-to-Value (LTV)

- LTV ratios typically fall between 65% and 85%. Government or USDA loans may allow up to 95% LTV for eligible applicants.

- A lower down payment can be negotiated with strong financial history, government guarantees, or proven sustainable management practices.

Sustainability and Environmental Clauses

- Increasingly, loans include environmental clauses encouraging or requiring sustainable land management, crop rotation, regenerative practices, and conservation projects.

- See Farmonaut’s carbon footprint monitoring solutions for actionable ways to track and maintain compliance with lender expectations.

- Accessing real-time environmental and resource data, via platforms like Farmonaut, enhances the borrower’s position for both loan qualification and management reporting.

How Farmonaut Supports Sustainable Farmland Management

Data-driven management is becoming a prerequisite for accessing the best farmland loan rates and terms in 2025. At Farmonaut, our mission is to make satellite-driven agricultural insights affordable and accessible worldwide, empowering farmers, businesses, and governments with actionable information for smarter farmland buying and management decisions.

- Fleet Management: Farmonaut Fleet Management solutions leverage real-time satellite and logistics data to optimize equipment usage, reduce operational costs, and demonstrate efficiency improvements—a key consideration for loan underwriters evaluating farm management capabilities.

- Crop Loan and Insurance: Using satellite-based crop loan verification tools, financial institutions streamline application and risk assessment for agricultural loans, making financing more accessible and reducing fraud risks for both lenders and borrowers.

- Blockchain Traceability: With traceability technology, farmers and agribusinesses can verify supply chain integrity, improving eligibility for preferential lending focused on transparency and regulatory compliance.

- Environmental Monitoring: Our carbon footprinting and real-time soil and water analysis tools provide evidence for compliance with lender sustainability requirements.

- API Access: For agribusinesses and agtech developers, the Farmonaut API and Developer Docs unlock seamless integration of rich, field-level satellite insights directly into your lending decision workflows.

The Future: Farming Loan Innovations & Market Outlook

The climate of farming loans in 2025 is increasingly shaped by innovation, data-centric management, and ecosystem-wide sustainability requirements. Here’s a look at the trends influencing save-savvy farmland loan rates and terms in today’s market:

- Loans for precision agriculture, renewable energy (solar, biogas), and certified organic/transition practices are seeing higher approval rates and discounted interest offers.

- Satellite monitoring and AI-based advisory (such as Farmonaut’s Jeevn AI) enable lenders to quickly verify farm productivity, ensuring more favorable terms for tech-enabled farms.

- Blockchain and supply chain traceability, as enabled by new technologies, can support eligibility for export-oriented or specialty crop-specific loans, especially where environmental stewardship reporting is mandatory.

- Government and private programs continue to offer guarantees, grants, or preferential rates for:

- Young and beginning farmers

- Land improvement projects (restoring wetlands, buffer planting, carbon sequestration)

- Environmental compliance (meeting new state, local, or international standards)

- Digital lending platforms are streamlining loan approvals and management, increasing access for rural borrowers and reducing administration times.

- Emerging climate risks are influencing rate-setting, with lenders more closely evaluating farm adaptability and resource resilience.

Frequently Asked Questions (FAQ) on Farmland Loans 2025

What are the average farmland loan rates in 2025?

Across major U.S. regions, farmland loan rates in 2025 typically range from 5.2% to 6.8%, though exact figures may vary by lender type and borrower profile.

What is the typical duration (term) for a farmland loan?

Farmland loan terms typically span 10 to 30 years, supporting long-term business planning and generational farm ownership structures.

How much down payment do lenders require for farmland loans?

Most lenders require a minimum down payment between 15% and 30%. However, government and USDA programs may accept as little as 5% for qualified borrowers.

What is the role of sustainability in farmland loan approval?

Lenders increasingly factor in sustainable farming practices and land management plans, often offering preferential rates for projects that enhance soil health, water efficiency, carbon sequestration, or biodiversity.

How can satellite technologies like Farmonaut help secure and manage farmland loans?

Farmonaut’s satellite solutions support loan qualification and ongoing management by providing real-time insights into crop health, soil conditions, environmental impact, and fleet operations, giving both borrowers and lenders confidence in the productive and sustainable use of agricultural land.

Where can I get digital tools and APIs to manage farmland and demonstrate compliance to lenders?

Explore Farmonaut’s Large Scale Farm Management digital monitoring app and API tools for seamless access to the reporting and data needed for best-in-class farm finance management.

Conclusion: Strategic Financing for Long-Term Growth

In 2025 and beyond, navigating farmland loans is both a science and an art—combining economic foresight, operational discipline, and a commitment to sustainability. By understanding current farmland loan rates, terms, and eligibility criteria, today’s entrepreneurs and farmers can unlock affordable, tailored financing to buy, expand, or improve their land with confidence.

With the support of innovative digital technologies—such as those offered by Farmonaut—lenders and borrowers alike gain unprecedented visibility and control. This ultimately elevates the security, accessibility, and environmental responsibility of agricultural finance, ensuring a resilient food system for years to come.

Ready to enhance your farmland financing journey?

Download the Farmonaut app or get started online to unlock actionable satellite and AI-powered farm insights: