Bad Credit Ag Loans & Farm Loans: Carbon Credit Market – Unlocking Sustainable Agri-Finance in 2025

Meta Description: Explore how bad credit ag loans and the carbon credit market for agriculture are driving financial inclusion, sustainable practices, and new opportunities for farmers and agribusinesses worldwide in 2025.

Introduction: The Intersection of Bad Credit Ag Loans & Carbon Credit Market in 2025

The intersection of bad credit ag loans and the carbon credit market for agriculture is reshaping opportunities, addressing challenges, and building a foundation for financial inclusion and sustainable practices in the worldwide agricultural sector as we approach 2025.

Amid growing climate change pressures and the need for environmental stewardship, farmers, especially those with bad credit histories, face a critical hurdle to accessing financial resources.

Traditional lending mechanisms, influenced by defaults stemming from past risks, offer little support to those with poor credit, often excluding tenant farmers, smallholders, and those impacted by volatile prices, weather variability, and systemic barriers.

Meanwhile, the carbon credit market for agriculture is burgeoning, offering an innovative avenue for farming operations to transform sustainable practices into tradable value.

By quantifying the environmental benefit of climate-friendly agricultural activities, this market rewards farmers for their carbon reduction and sequestration efforts.

When layered with evolving bad credit ag loans that incorporate alternative data and government-backed schemes, a dynamic synergy emerges—one that can help mitigate risk, stabilize incomes, and enhance creditworthiness.

In this comprehensive guide, we unravel how these mechanisms operate individually and collectively.

We explore current trends, outline the main challenges, spotlight emerging opportunities, and—using authoritative data—outline actionable insights for stakeholders in farming and agribusinesses worldwide.

Bad Credit Ag Loans in 2025: Bridging the Financial Gap

Why Farmers Face Credit Barriers

Agriculture is inherently risky.

Farmers face an array of risk factors:

- Weather variability: Unpredictable rainfall, drought, and extreme events threatened crop yields.

- Pest outbreaks and diseases: New and more resilient pests can devastate crops.

- Volatile prices: Fluctuating commodity markets and global trading disputes directly impact farm incomes.

- Past defaults stemming from unfavorable seasons or market shocks hurt future creditworthiness.

- Systemic issues that keep tenant farmers and smallholders outside conventional banking and lending circles.

The Rise of Bad Credit Ag Loans

Bad credit ag loans and bad credit farm loans have gained fresh traction in 2025,

thanks to specialized financial products developed to serve farmers who:

- Do not meet conventional criteria due to fluctuating incomes or defaults

- Have poor credit histories but require capital to start, scale, or sustain farm operations

- Are recovering from setbacks like pest outbreaks, weather disasters, or market price slumps

- Are tenant farmers or smallholders with limited access to formal credit systems

Key Features of Bad Credit Ag Loans in 2025:

- Alternative data: Lenders now assess risk using farm production records, crop insurance policies, commodity sales history, and digital footprints in addition to credit scores.

- Government-backed guarantees: Credit guarantee schemes help lenders reduce default risk and offer better lending terms.

- Flexible loan structures: Terms may include more lenient collateral requirements and income-contingent repayments.

- Digital access: Mobile and online loan applications make bad credit ag loan processes more accessible for remote and underbanked communities.

How Bad Credit Farm Loans Support Sustainable Practices

A significant trend is the integration of sustainability metrics into bad credit farm loans. Increasingly, lenders are incentivizing farming practices that contribute to climate change mitigation and environmental outcomes—such as embracing conservation tillage, cover cropping, or regenerative agriculture.

Farmers who meet sustainability-linked terms may qualify for:

- Lower loan rates

- Access to technical assistance and AI-based advisory services

- Eligibility for government or private credits tied to environmental performance

Farm Finance in 2025: Lending Models and Trends

- Credit Guarantee Schemes: Government and multilateral agencies are expanding such schemes, which mitigate lender risk for bad credit ag loan portfolios.

- Microfinance Institutions: These institutions offer group-based loans that rely on peer monitoring, enabling financial inclusion for unbanked smallholders.

- Sustainability-Linked Loans: Some lenders use carbon sequestration or emissions reductions—validated within the carbon credit market—as a condition for more flexible loan terms.

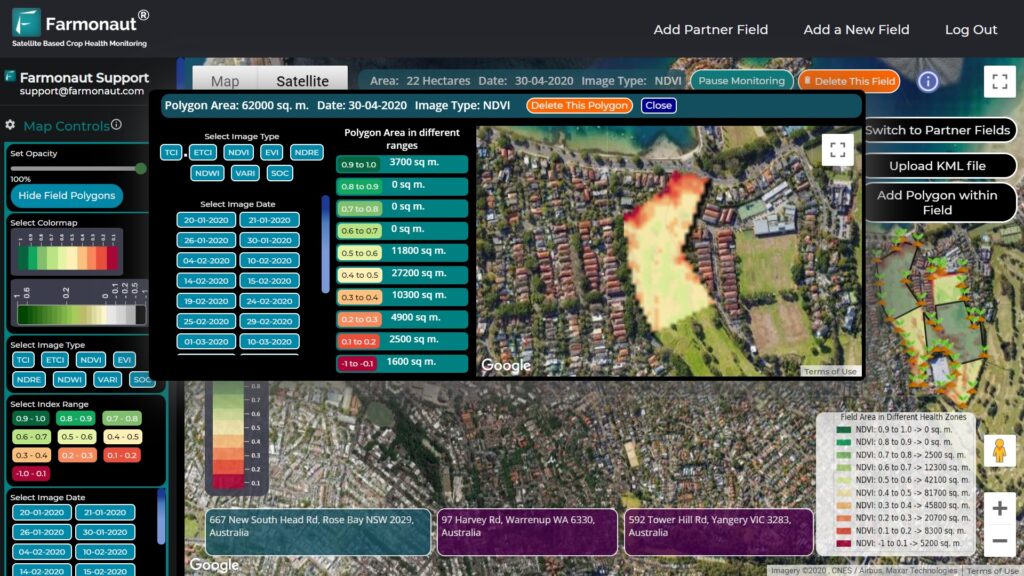

- Embedded Tech Verification: Satellite and AI-based farm monitoring—like those available through Farmonaut (see more below)—help lenders verify land use, crop production, and eligibility for credit-linked environmental incentives.

Learn about Farmonaut’s Satellite-Based Verification for Crop Loans & Insurance – supporting lenders and farmers by reducing fraud, increasing transparency, and unlocking better financing rates.

The Carbon Credit Market for Agriculture: A Sustainable Financing Avenue

The carbon credit market for agriculture represents a valuable complement to traditional loans and is a fast-growing avenue for farm incomes in 2025.

Carbon credits are tradable certificates representing the reduction or sequestration of one metric ton of carbon dioxide equivalent (CO₂e)—a crucial innovation for mitigating climate change at scale.

How the Carbon Credit Market Works

- Identification of Sustainable Practices: Farmers adopt climate-smart methods like agroforestry, reduced tillage, cover cropping, or methane management from livestock.

- Measurement, Reporting, Verification (MRV): Sophisticated models and satellite-based MRV solutions now allow more accurate accounting of carbon reductions or sequestration.

- Certification: Independent bodies issue tradable carbon credit certificates based on validated data.

- Trading: Credits are sold to buyers—either corporations (seeking to offset their emissions) or governments—on regulated or voluntary carbon markets.

- Revenue: Farmers earn an additional income stream directly linked to their environmental stewardship.

Key Developments in 2025:

- Structured Markets: Improved regulations and transparent pricing boost farmer confidence.

- Lower Transaction Costs: AI-driven verification models and blockchain-based traceability streamline certification.

Learn about Farmonaut’s end-to-end Blockchain Traceability – ensuring transparency, data integrity, and accessible, auditable carbon credits for every farm product. - Digital Platforms: Mobile/web-based tools help farmers access carbon credit programs anywhere, improving inclusion.

- Integration With Loan Repayments: Some lenders now allow the use of carbon revenue to repay agricultural loans.

The environmental benefits of participating in the carbon credit market for agriculture include:

- Reduction in greenhouse gas emissions (carbon dioxide, methane, nitrous oxide)

- Improved soil health and resilience to climate extremes

- Added revenue supporting farm resilience and rural development

- Stronger market positioning for meeting ESG (Environmental, Social, and Governance) standards and supply chain expectations

Making Carbon Markets Accessible for All Farmers

Despite their promise, technical and bureaucratic hurdles can hinder smallholder and tenant farmer access to carbon credit markets. Key challenges include:

- High transaction costs for verification, certification, and market participation

- Lack of awareness and technical know-how

- Limited aggregation mechanisms for small farms

- Difficulty demonstrating actual impact in complex farming systems

Still, 2025 advancements in digital MRV technology—such as Farmonaut’s AI-driven environmental impact monitoring—are leveling the playing field (see more below).

The Synergy Between Bad Credit Ag Loans & the Carbon Credit Market

A Game-Changer for Financial Inclusion and Sustainability

The synergy between bad credit ag loans and the carbon credit market for agriculture is transformative for the global farming sector.

- Lenders provide borrowers with financing contingent on sustainable practices, using alternative data like carbon sequestration scores and satellite-based monitoring to holistically assess farm viability.

- Farmers use carbon revenue to strengthen cash flow, pulling them out of “bad credit” categories towards regular financing.

- The combination encourages environmental stewardship, financial stability, and resilience to climate-related risks.

- Participating farmers improve their creditworthiness by demonstrating reliable alternative income and commitment to sustainability.

Examples of Emerging Models:

- Bundled Loan-Carbon Credit Packages: Lenders tie loan terms and rates directly to measured improvements in carbon reduction or sequestration (as tracked via MRV platforms).

- Revenue Sharing: A portion of carbon credit proceeds is funneled back to repay ag loans, reducing default risk and improving financial inclusion.

- Transition Support: Low-credit farmers eventually qualify for traditional loans as their financial and sustainability footprints improve.

Collectively, these mechanisms are reshaping opportunities for stakeholders in farming and agribusiness worldwide—improving both economic and environmental outcomes.

Comparative Impact Table: Loans and Carbon Credit Participation

| Farmer Type | Access to Carbon Credit Programs | Estimated Annual Loan Rate (%) | Estimated Increase in Farm Revenue ($, 2025) | Estimated Sustainability Score (1-10) | CO₂ Offset Potential (tons/year) |

|---|---|---|---|---|---|

| Bad Credit Loan + Carbon Credit Participation | Yes | 7.5–11 | $6,000–$20,000 | 8–10 | 55–350 |

| Bad Credit Loan Only | No | 11–15 | $2,000–$5,000 | 5–7 | 0–50 |

| No Loan, With Carbon Credit Participation | Yes | 0 | $4,000–$10,000 | 7–9 | 40–230 |

| No Loan, No Carbon Credit Participation | No | 0 | $1,000–$3,000 | 3–6 | 0–25 |

* Figures are illustrative estimates for 2025 based on current market research and sector projections. Actuals vary by location, farm size, and practice type.

Farmonaut Solutions: Accelerating Sustainable & Financially Inclusive Agriculture

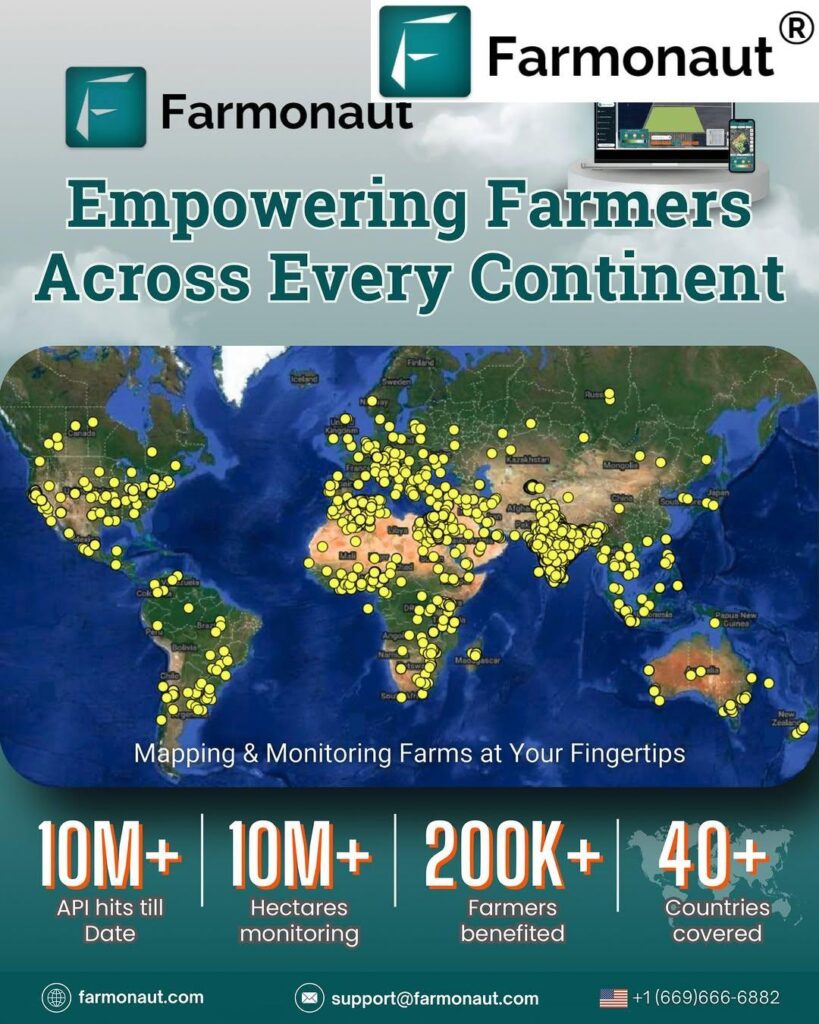

As a pioneering satellite technology company, we at Farmonaut empower the intersection of bad credit ag loans and the carbon credit market for agriculture with advanced, accessible technology. Our mission is to democratize actionable data for farmers, lenders, businesses, and governments worldwide.

Transformative Technologies for 2025 and Beyond

-

Satellite-Based Crop & Soil Monitoring: We use multispectral images to deliver real-time insights on crop health (NDVI), soil moisture, and field variability.

This data supports farmers and lenders in holistically assessing creditworthiness and identifying opportunities for carbon reduction/sequestration. - Jeevn AI Advisory System: Our AI-driven system analyzes field data and weather trends to deliver actionable, field-specific guidance—helping maximize both yield and resource use while empowering sustainable practices.

-

Blockchain-Based Traceability: We offer secure, tamper-proof tracking for carbon credits, supply chain flows, and farm outputs, supporting rankings for both loan eligibility and market access.

Discover Farmonaut’s Traceability Tools for Carbon and Crop Markets -

Environmental Impact Monitoring: Our platform tracks carbon footprinting and emission reductions in real time for both lenders and individual operations.

Explore Farmonaut’s Carbon Footprinting Solutions – ideal for verifying metrics in the carbon credit market for agriculture. -

Subscription & API Access: Our cost-effective app, web dashboard, and robust API provide instant access to the latest data for all stakeholders—plus full mobile compatibility.

See Fleet Management Solutions from Farmonaut – optimize machinery, logistics, and reduce operating costs with real-time tracking.

Manage Large Scale Farms Using Farmonaut’s Agro Admin App – streamline field operations, monitor outcomes, and scale success across regions.

For developers and integrators:

• Explore the Farmonaut API – connect satellite insights to any agricultural, credit, or carbon management workflow.

• API Developer Docs Here.

Challenges & The Way Forward in Agri-Finance and Carbon Credits

The Remaining Hurdles

Despite the advancements highlighted above, farmers, lenders, and policymakers must continue addressing key challenges for sustained impact:

- Measurement, Reporting, and Verification (MRV): Even with satellite, AI, and blockchain innovations, the accuracy and trustworthiness of MRV for carbon credits remains a crucial issue—especially for highly diversified or small-scale farms.

- Technical and Bureaucratic Barriers: Smallholders and tenant farmers often lack the skills, connectivity, or knowledge to access advanced ag loans and carbon markets on their own.

- Cost & Aggregation: The fixed transactional costs of carbon market participation are lower in 2025, but may still deter the smallest players unless aggregation (e.g., via cooperatives) solutions are scaled.

- Lender Risk Models: Credit risk assessment models must continue improving to incorporate environmental and alternative financial data accurately, balancing risk reduction with financial inclusion.

Policy support and sustained investment in technical assistance programs are critical. Governments and private sectors should invest in:

- Expanded credit guarantee schemes and blended finance for bad credit ag loans

- Technical/educational support for climate-smart agriculture and carbon program participation

- Public-private partnerships to promote farmer aggregation for carbon projects

- Research and innovation to enhance digital MRV models (for example, support for platforms like Farmonaut’s AI-based monitoring)

The Way Forward for 2025 and Beyond

As climate change pressures mount and environmental regulation tightens worldwide, status quo approaches will not suffice.

The co-evolution of bad credit ag loans and the carbon credit market for agriculture offers a roadmap for a

resilient, inclusive, and sustainable agriculture sector.

- Lenders and policymakers must continue building inclusive, technical, and flexible financial products tied to environmental outcomes.

- Carbon credit markets must evolve with robust digital infrastructure, supporting credible, accessible programs that empower all farmer segments.

- Farmers should embrace digital MRV, collaborative program models, and seek technical support to maximize both profitability and sustainability.

Platforms like Farmonaut will play an essential role in enabling this vision through affordable, accessible technology for all stakeholders in 2025 and beyond.

FAQs on Bad Credit Ag Loans & The Carbon Credit Market

What are bad credit ag loans, and who qualifies for them?

Bad credit ag loans are specialized financial products tailored for farmers and agricultural operators who do not qualify for traditional bank loans due to poor credit scores, past defaults, or lack of standard collateral. Qualification focuses on alternative data like farm production records, crop insurance, and commodity sales history.

How do carbon credits benefit farmers with bad credit?

Carbon credits allow farmers to generate an additional income stream by adopting sustainable practices that reduce or sequester greenhouse gases. This revenue can help repay loans, improve creditworthiness, and stabilize financial outcomes for farmers typically excluded from conventional finance.

What technological solutions enhance access to loans and carbon market programs?

Platforms like Farmonaut provide satellite monitoring, AI advisory, blockchain traceability, and mobile/web apps. These tools support reliable measurement, reporting, and verification for carbon credits and enable lenders to more accurately assess risk for bad credit farm loans.

Are there risks involved in linking loans to carbon credits in 2025?

While revenue diversification and improved sustainability scores are positives, carbon markets are still evolving and may carry price volatility and regulatory risks. Loan agreements must be flexible, and farmers should seek guidance from technical assistance programs or advisors.

What’s the best way for small-scale farmers to access carbon credits?

Join farmer cooperatives or aggregation programs, use digital platforms for MRV participation, and leverage affordable technology like those from Farmonaut for environmental monitoring and data collection.

Conclusion: The Future of Sustainable Agri-Financing

Looking ahead to 2025 and beyond, the integration of bad credit ag loans and the carbon credit market for agriculture is crucial for bridging the financial gap, driving inclusion, and accelerating the shift towards sustainable farming practices worldwide.

By harnessing new technical models, digital verification, and innovative lending frameworks, we empower farmers and agribusinesses to achieve greater resilience, profitability, and environmental stewardship.

It is imperative that policymakers, lenders, and technology providers continue improving models, reducing costs, and expanding access—to ensure every farmer, regardless of past setbacks or credit histories, can thrive in a climate-resilient, inclusive future.

As a trusted platform, we at Farmonaut are dedicated to supporting this transition with cost-effective, data-driven solutions designed for real-world impact across the agricultural sector.

Ready to transform your farm finance and sustainability outcomes?

Start your journey with Farmonaut’s platform today—even for bad credit ag loans and carbon market participation in 2025!